The End of the Premium Card Honeymoon: Why HDFC Infinia and Others Are Tightening the Screws on Rewards – And What It Means for Indian Cardholders

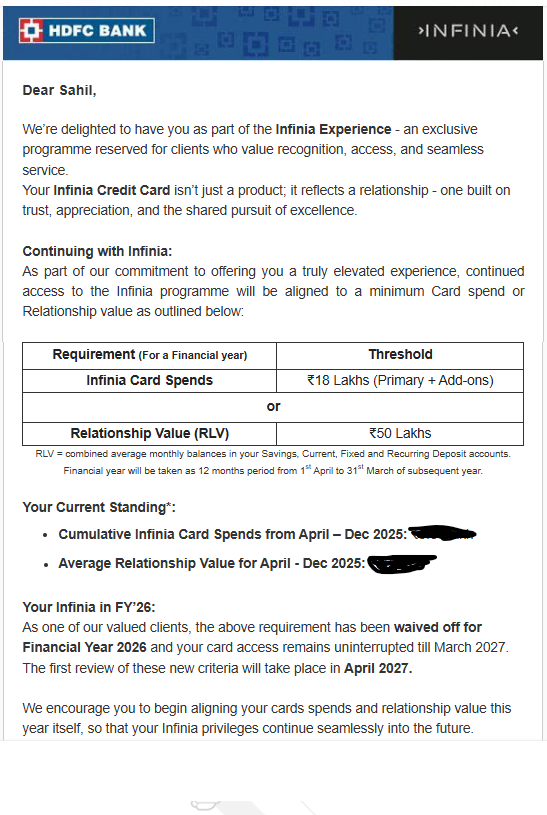

In the world of premium credit cards in India, HDFC Bank’s Infinia has long been the crown jewel – a symbol of luxury, unlimited lounge access, and unbeatable reward points. But recent changes, as outlined in emails sent to cardholders, signal a seismic shift. Starting from the financial year 2027 (April 2026–March 2027), Infinia users must now hit either ₹18 lakh in annual spends (across primary and add-on cards) or maintain a ₹50 lakh Relationship Value (RLV) – essentially the average monthly balance across your HDFC savings, current, fixed, and recurring deposits. For FY26, these requirements are waived, giving you uninterrupted access until March 2027. But after that? Miss the mark, and you risk downgrade or loss of privileges.

This isn’t just HDFC’s move – it’s part of a broader trend where banks are “devaluing” their once-generous reward programs. From Axis Bank’s Magnus nerfs in 2024 to similar tweaks across the industry, banks are forcing higher spends or balances to keep the lights on. But why now? And is it fair that a few reward-chasers are spoiling the party for genuine high-net-worth users? Let’s break it down for DealUni readers, exploring the reasons, the fallout, and better alternatives in today’s market.

Why Are Banks Suddenly Demanding More Spends and Balances?

Credit card rewards aren’t free – they’re funded by interchange fees (what merchants pay banks for transactions), annual fees, and interest on unpaid balances. For years, banks like HDFC and Axis aggressively marketed premium cards like Infinia and Magnus to a wide audience, often with low barriers to entry. Infinia, for instance, was invite-only but extended to many with solid credit histories and relationships, boasting up to 33% effective returns on travel bookings via SmartBuy. The pitch? Unlimited rewards, golf games, lounge access, and more – all for a ₹12,500 annual fee that could be waived with ₹8-10 lakh spends.

But here’s the rub: As more users “exploited” these programs – think manufacturing spends through vouchers, utilities, or even rent payments to max out rewards – banks’ costs skyrocketed. Reward points became a liability when redeemed en masse for flights, hotels, or cash equivalents. To stem the bleed, banks devalue programs by capping rewards, hiking requirements, or reducing redemption values. For Infinia, the new thresholds ensure only “profitable” customers – those who spend big or park serious money with the bank – stick around.

This mirrors global trends: In the US, issuers like Chase and Amex have similarly tightened lounge access and transfer ratios as programs grew unsustainable. In India, rising credit card debt (over ₹33,886 crore as of late 2025) and regulatory scrutiny from RBI on unchecked lending have pushed banks to refocus on high-value relationships. As one X user noted in discussions around Infinia changes, “Banks are trimming the portfolio to keep equity with real cardholders who keep the lights on.”

The Cycle: Easy Access, Exploitation, and Crackdown

Banks initially “give cards to everyone” to scale quickly and capture market share. HDFC pushed Infinia as an “elevated experience” for those valuing “recognition and access,” while Axis Magnus was marketed with 5:4 transfer ratios that could yield 25-50% returns on optimized spends. This democratized premium perks, but it backfired when savvy users gamed the system – buying vouchers in bulk, paying utilities for points, or even cycling spends to hit milestones without real economic value to the bank.

The turning point? Axis Magnus’s major devaluation in May 2024: Monthly milestones of 25,000 bonus points were axed, accelerated rewards capped at credit limit + ₹1.5 lakh, and transfer ratios adjusted. X threads exploded with frustration, with users calling it the “devaluation of the year.” HDFC followed suit with Infinia tweaks, like limiting reward redemptions to five per month from February 2026 and now these retention criteria. As one forum post put it, “Axis started the devaluation, and slowly other banks… have started crawling them back.”

It’s a classic bait-and-switch: Lure with lucrative offers, then restrict once hooked. But as the user aptly quoted, “When something is given free for long or at unbelievable price, it has to go away someday or the other.” Infinia was the undisputed king, offering one of the best reward rates in India (up to 5 points per ₹150, redeemable at 1:1 for flights/hotels). Now, it’s aligning with sustainability.

Is What Banks Are Doing Right? The Fairness Debate

On one hand, yes – banks aren’t charities. Devaluations protect their bottom line from “arbitrageurs” who exploit loopholes without building real relationships. As X discussions highlight, “Magnus was always for high spenders,” and these changes reward genuine big-ticket users while weeding out low-engagement holders. Ethical? From a business standpoint, absolutely – mid-term changes like ICICI’s Emeralde devaluation (cash conversion from 1:1 to lower within a month) show banks prioritizing profits.

But no, it’s not fair when a few exploiters lead to blanket restrictions, hurting “genuine people.” Many Infinia holders with moderate spends (e.g., ₹50k monthly) now face downgrade risks, as one Reddit user lamented: “Infinia setting up a 18L yearly criteria will mean I may be out.” Broader context: India’s shift to consumption-driven debt (112 million cards, rising defaults) punishes savers while banks hike minimum balances (e.g., ₹50k in metros, penalizing the poor). X sentiments echo this: “Because of few cc holders other genuine people will suffer.” Regulators like RBI could mandate better notice periods, but for now, users bear the brunt.

Better Cards Than Infinia? Yes, Plenty in 2026

Infinia’s throne is wobbling – with devaluations, alternatives shine brighter for high spenders. Here’s a comparison of top premium cards in India for 2026, based on rewards, fees, and perks:

| Card | Annual Fee (Waiver) | Key Rewards | Best For | Why Better Than Infinia? |

|---|---|---|---|---|

| Axis Magnus Burgundy | ₹30k + GST (waived on ₹30L spends) | ~4.8% base, up to ~14% on milestones; Accor transfers double value | High spenders (₹1.5L+/month) | Higher uncapped potential post-₹1.5L; better for miles game. |

| HSBC Premier | Varies (often LTF for eligible) | ~3% base, ~18% flights, ~36% hotels; Accor doubles | Frequent travelers | Superior hotel/flight returns without spend caps; more flexible transfers. |

| ICICI Emeralde Private Metal | ₹12,500 + GST | Unlimited golf/lounge; 2-6% rewards | Luxury perks | Broader insurance, no redemption limits; similar to Infinia but with metal appeal. |

| HDFC Diners Black Metal | ₹10k + GST (waived on ₹8L spends) | ~3.33% base, up to 33% hotels; 10k bonus quarterly | Balanced spenders | Cheaper entry, similar SmartBuy boosts; milestone bonuses edge out Infinia for mid-tier. |

| Axis Atlas | ₹5k + GST | Tier-based miles (up to 5 per ₹100); 1:1 transfers | Air miles focus | Lower fee, uncapped on flights; post-devaluation resilience. |

These cards often outperform Infinia on specific categories, especially if your spends align with travel or milestones. As one Instagram reel ranked: “Magnus Burgundy is number one… Infinia is the worst” in head-to-heads.

Final Thoughts: Adapt or Downgrade?

The era of “unbelievable” freebies is fading – Axis kicked it off with Magnus in 2024, and HDFC’s Infinia move is the latest domino. Banks are right to protect viability, but the collateral damage on genuine users stings. If you’re below the thresholds, start ramping spends or balances now, or explore downgrades like HDFC’s Diners Black. For alternatives, focus on cards matching your habits – miles for travelers, cashback for everyday.

At DealUni, we track these shifts to help you maximize deals. What’s your take? Share in the comments – and if Infinia’s your ride-or-die, redeem those points before more changes hit!